Download the PDF

Australian superannuation funds face a complex set of challenges in 2026. The outlook for equity returns remains sensitive to market, economic and policy conditions, while persistent inflation is reinforcing the need for diversification across a range of scenarios. At the same time, increasing allocations to offshore and unlisted assets have heightened liquidity management requirements. Identifying return sources that can contribute meaningfully to performance, provide diversification and preserve liquidity is a growing priority for asset owners.

Derivative overlays offer a practical way to access uncorrelated, liquid and scalable return streams without the structural drawbacks often associated with hedge funds, such as high fees, limited transparency and capacity constraints. Implemented within a well-governed framework, derivatives-based alpha programs can complement existing portfolio allocations while maintaining alignment with liquidity and risk objectives.

This paper explores the case for using derivatives to generate alpha and sets out practical, illustrative strategies for implementing an alpha program.

This paper is part of a four-part series exploring how Australian institutional investors are using derivatives.

- Derivatives for alpha

- Derivatives for exposure management

- Derivatives for risk management

- Derivatives for liquidity management

Market context

When setting allocations, institutional investors need to balance a range of competing objectives. Optimising diversification, fees, liquidity and performance often involves trade-offs. For example, increasing exposure to unlisted assets may reduce equity concentration, but it can also reduce short-term liquidity. The challenge is improving the overall portfolio without creating new pressures elsewhere.

The evolving macro landscape is adding to these challenges. Shifts in inflation regimes and market structure have underscored the potential for changing correlations, challenging traditional assumptions around portfolio diversification. As portfolios have evolved to meet these challenges, it has become increasingly difficult to identify novel return streams that provide uncorrelated performance, that can be scaled and customised to suit individual portfolio goals and constraints. Investors are increasingly adapting to this environment by seeking out additional sources of alpha1, including those available in derivative markets.

Derivatives as a solution

Institutional investors have long relied on derivatives for risk management, with currency hedging and cash equitisation being well-established practices. Today, these same instruments can be applied to generate alpha in a way that is capital-efficient, transparent and scalable.

Unlike traditional allocations, derivatives typically require only partial funding, freeing capital for other uses while maintaining liquidity. Positions can be sized to suit risk budgets rather than capital constraints, allowing overlays to scale with fund growth or adapt to changing market conditions. Derivatives also provide agility, with exposures adjusted quickly and cost-effectively, enabling investors to capture short-term opportunities without disrupting core allocations. This flexibility can help investors meet the competing objectives of portfolio construction.

Importantly, derivatives can provide exposures that are difficult or impractical to access in physical markets (e.g. commodities). This flexibility broadens the alpha universe and supports diversification objectives. Combined with the ability to implement market-neutral or relative-value strategies, derivatives offer a compelling way to introduce novel return streams into institutional portfolios.

Positions can be sized to suit risk budgets rather than capital constraints, allowing overlays to scale with fund growth or adapt to changing market conditions.

Why demand for derivatives is increasing

- Correlations of stocks and bonds are less certain: The re-emergence of inflation has highlighted the need for investments that complement the traditional mix of equities and bonds.

- Greater uncertainty around equity return outcomes: Equity returns are increasingly influenced by changes in market structure, leadership and dispersion across sectors and regions. This has sharpened the focus on managing return expectations and sourcing differentiated drivers of performance.

- Greater pressure on liquidity: The increasing focus on liquidity combined with a growing stock of unlisted assets increases the need for portfolio tools that can generate alpha with minimal liquidity consumption.

- Novel return streams: Asset classes have evolved to cover a wide range of often complex strategies. It is becoming harder to find opportunities that are unique, scalable and uncrowded in institutional portfolios.

Drivers of alpha opportunities

Alpha opportunities in derivatives markets are driven by a combination of structural, regulatory and behavioural factors, which can create pricing inefficiencies and, in turn, potential investment opportunities.

Understanding these drivers is critical in assessing how reliable and scalable different strategies may be.

- Structural imbalance: Regulatory changes and dealer balance-sheet constraints have altered risk intermediation, creating opportunities for well-capitalised investors. Example: US Treasury cash-futures basis.

- Transitory dislocations: Policy surprises, crowded positioning and liquidity frictions can create episodic mispricing. Example: rates basis markets around issuance windows.

- Regulatory drivers: Post-crisis regulation has reduced the ability of banks to undertake some activities, which can result in attractive pricing for counterparties willing to assume risk. Example: increased funding costs around year-ends.

- Non-economic participants: Hedging flows and policy-driven transactions can create opportunities for profit-motivated investors. Example: cross-currency basis markets trading cheap or rich.

These dynamics are not uniform across markets, but they provide a foundation for strategies that seek to capture risk premia or exploit temporary inefficiencies. A well-structured derivatives program can help institutional investors access these opportunities within a disciplined risk framework.

Benefits of derivatives for institutional investors

- Capital efficient: Futures, swaps and options typically require initial and variation margins rather than full funding2, helping to preserve liquidity and minimise disruption to existing allocations.

- Scalable: Positions can be sized to suit risk budgets and governance limits, allowing exposures to grow with total assets or developing strategies to expand.

- Agile: Exposures can be adjusted quickly and cost-effectively, enabling investors to target temporary or episodic opportunities without disrupting core allocations.

- Diversified: Investors can take long and short exposures, allowing investments to be structured with minimal sensitivity to traditional asset classes or risk factors.

- Novel return streams: By providing access to exposures unavailable in physical markets, derivatives broaden the alpha universe without impacting core holdings and existing asset sectors.

- Opportunistic: A derivatives overlay can be scaled up or down quickly to suit the opportunity set, with minimal drag from uninvested capital.

Illustrative strategies for alpha generation

Structural features in derivatives markets can create return opportunities. These opportunities can vary widely, reflecting both the breadth of derivative markets and the range of structures available within them.

Each major listed asset market typically has an associated derivatives market, within which investors can use a range of instruments, including options, swaps and futures. To demonstrate the types of opportunities available, we outline two illustrative strategies below. These examples are not intended as investment recommendations, but are designed to highlight key concepts and considerations relevant to strategy selection.

Example 1: Volatility risk premium (VRP)

A volatility risk premium strategy seeks to capture the difference between implied volatility, reflected in option prices, and the realised volatility of the underlying asset. Historically, options have tended to trade at a premium to realised volatility, creating a potential opportunity for systematic sellers of volatility.

Key considerations

Rationale: Demand for downside protection and investor risk aversion often lead option prices to embed a volatility premium.

Risk characteristics: Performance can be positively correlated with equity markets during periods of stress, requiring careful sizing and risk controls.

Implementation: Exposure can be accessed through listed options or structured products. Position sizing can be based on risk measures or volatility parameters rather than notional capital.

Liquidity: Listed options markets are generally liquid, but margin requirements and episodic volatility spikes must be managed.

Complexity: Effective implementation requires strong risk management and close monitoring of market conditions.

Example 2: Equity total return futures (TRF) term structure

This strategy seeks to exploit different funding rates across the equity repo curve by taking offsetting positions across different TRF maturities. Equity funding rates reflect a range of factors including funding conditions and demand for synthetic exposure. Variations in these factors across the curve can result in funding rates at certain maturities trading cheap or rich relative to others, creating opportunities for relative-value investors.

Key considerations

Rationale: Curve pricing is influenced by factors including dealer balance sheet costs, financing demand, hedging activity and the supply–demand balance for synthetic equity exposure across maturities. These dynamics can lead to persistent pricing differences across the curve.

Risk characteristics: The strategy can be designed to be largely market-neutral, with performance impacted by changes in funding spreads, curve dynamics and periods of market stress. Careful risk management is required to manage basis volatility and potential funding shocks.

Implementation: Exposure is typically implemented by entering into offsetting equity TRF positions across the curve. With the repo curve bias being upward sloping, one strategy is to receive higher and longer dated repo rates by selling TRF contracts, while offsetting the position with shorter tenor TRF contracts. This implementation style seeks to exploit the carry and rolldown of the equity repo curve.

Liquidity: Equity TRF markets are less liquid than equity index futures, requiring positions and trading to be managed accordingly. Liquidity and pricing can vary across tenors and market conditions.

Complexity: Effective implementation requires robust risk management and ongoing monitoring of futures positions and funding levels.

Designing a scalable alpha overlay

The factors outlined above explain why return opportunities exist in derivatives markets and the types of strategies that may be used to capture them. However, derivative-based strategies exhibit specific features, such as partial funding, daily liquidity requirements and the potential for non-linear payoffs, that require dedicated infrastructure to manage effectively.

While these characteristics can appear operationally complex, when embedded within a well-designed alpha overlay, they allow investors to access differentiated return sources with capital efficiency and transparency, without the need to build or maintain a full internal derivatives platform. In this sense, a scalable overlay provides a middle ground between allocating to standalone hedge funds and developing wholly internal capabilities.

A clear governance and risk management framework remains essential, but it is typically established ex ante and embedded within the overlay mandate. Day-to-day implementation, monitoring and operational processes are delegated to the manager, while the asset owner retains control over objectives, constraints and portfolio integration.

Key design considerations include:

Overlay structure: The program can sit within an asset class sector or at the total portfolio level. The latter often suits multi-asset strategies and facilitates alignment with dynamic asset allocation processes and the availability of liquidity.

Funding and liquidity: Partial funding enhances capital efficiency, with liquidity, margining and stress buffers managed within the overlay to avoid operational burden on the broader portfolio.

Risk sizing: Allocations are expressed through agreed risk budgets, such as tracking error or volatility targets, allowing the overlay to be sized consistently with total portfolio risk objectives rather than capital allocations.

Instrument universe: A pre-defined, scalable instrument set balances flexibility with operational simplicity, avoiding the complexity typically associated with hedge fund strategies.

Constraints and objectives: Clear ex ante guidelines for return objectives, beta limits and exposure caps ensure the overlay remains tightly aligned with the fund’s broader portfolio objectives and governance framework.

Designed in this way, a scalable alpha overlay allows asset owners to access derivative-based return opportunities with a high degree of transparency, portfolio integration and capital efficiency, without requiring the investment team to operate derivatives strategies internally or rely on less integrated external hedge fund allocations.

Case study: Alpha overlay

The previous sections set out the case for using a derivatives program to generate alpha, as well as the key considerations for designing a program. The case study below illustrates how an Australian asset owner might structure a derivatives overlay targeting uncorrelated alpha.

Scenario

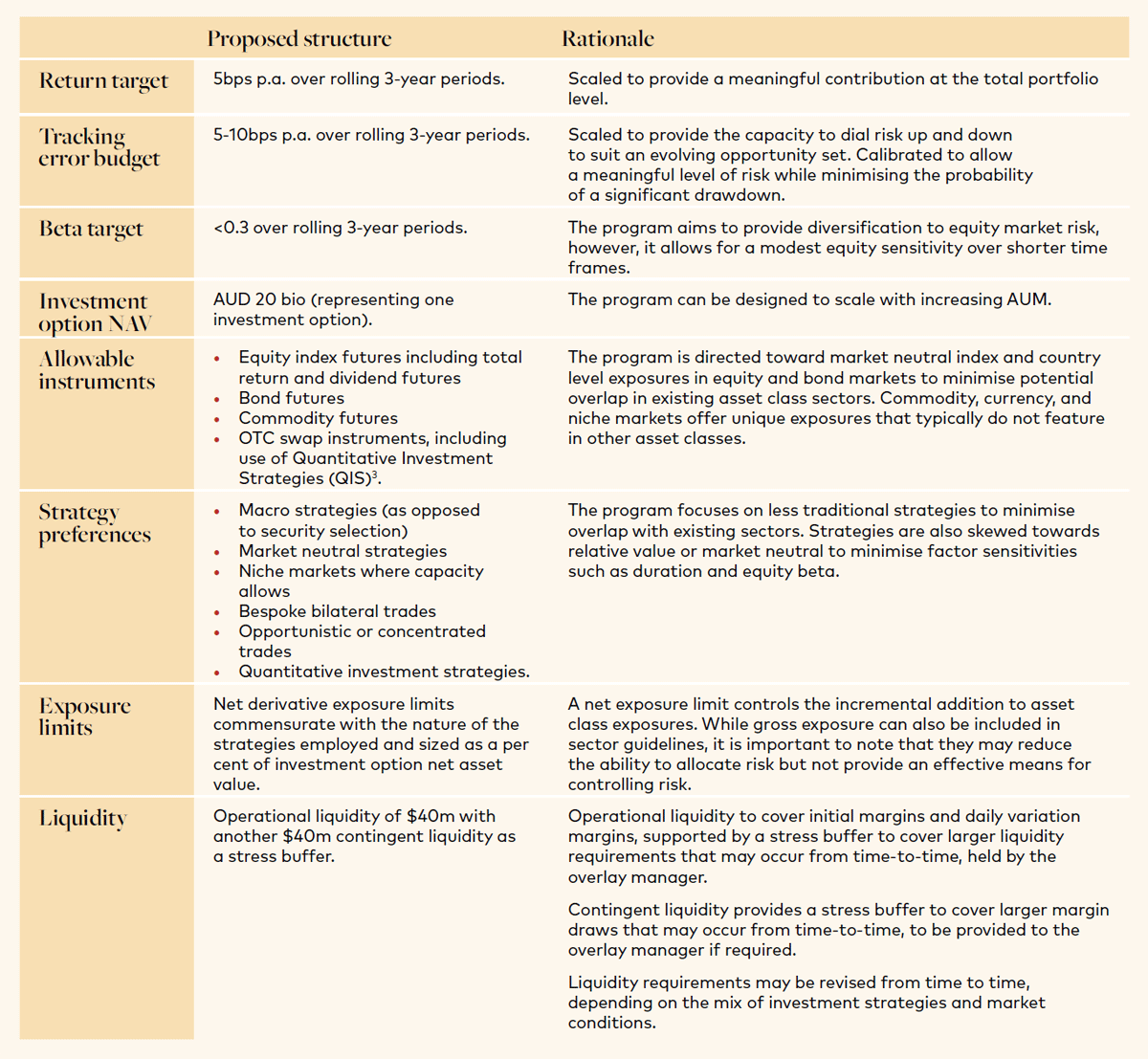

An Australian superannuation fund is seeking an investment return stream to increase diversification across its investment options. The fund’s main balanced option has assets of AUD 20 billion.

The preferred strategy would have:

- Minimal liquidity requirements, allowing the fund to maintain its physical asset allocation.

- A risk budget that is flexible enough to scale up or down to suit the opportunity set.

- Performance largely uncorrelated to the wider portfolio, although a modest level of equity beta is acceptable.

- Candidate investments distinct from those used elsewhere in the portfolio.

The fund currently includes a dynamic asset allocation (DAA) process targeting a tracking error (TE) of 50 bps p.a. at the investment option level. Its existing portfolio structure allows the use of futures in line with its DAA strategy, as well as over-the-counter swaps.

A potential approach is outlined in the following table.

This case study is provided for illustrative purposes only and is based on theoretical and simulated performance. The results shown do not represent actual trading and are not based on the performance of any QIC client portfolio. The analysis is shown gross of fees and costs, which would reduce returns if applied in practice. Past performance is not a reliable indicator of future performance.

This case study is provided for illustrative purposes only and is based on theoretical and simulated performance. The results shown do not represent actual trading and are not based on the performance of any QIC client portfolio. The analysis is shown gross of fees and costs, which would reduce returns if applied in practice. Past performance is not a reliable indicator of future performance.

Conclusion

Derivative overlays provide institutional investors with a practical way to broaden their alpha toolkit at a time when traditional return sources are under pressure. Their capital efficiency, liquidity preservation and ability to access both structural and episodic opportunities can open up return streams that are harder to access in physical markets.

With clear governance and disciplined risk management, these features can support scalable, uncorrelated alpha. For Australian institutional investors navigating elevated valuations, shifting correlations and growing liquidity demands, a well designed derivatives overlay can complement existing allocations and strengthen long term portfolio resilience.

Citations

- futurefund.gov.au/news-room/20230427---Keynote-by-Dr-Raphael-Arndt---Alpha-Live-Conference

- Margining is a highly nuanced topic with exact requirements varying across instruments and definitions. For example, while option premiums may be fully funded, the premiums are typically only a fraction of the underlying notional exposure.

- QIS are rules-based strategies designed to capture systematic market characteristics such as carry, trend, or volatility premia. Banks typically offer these strategies via OTC swaps linked to proprietary or public indices.