Download the PDF

The Basis is a quarterly presentation series by our Liquid Markets Group’s Multi-Asset Solutions team providing investors with insights into derivative structures and strategies, portfolio construction and other whole-of-portfolio investment topics.

In this edition, we dive deeper into one of the topics in this quarter’s The Basis: the benefits of duration hedging.

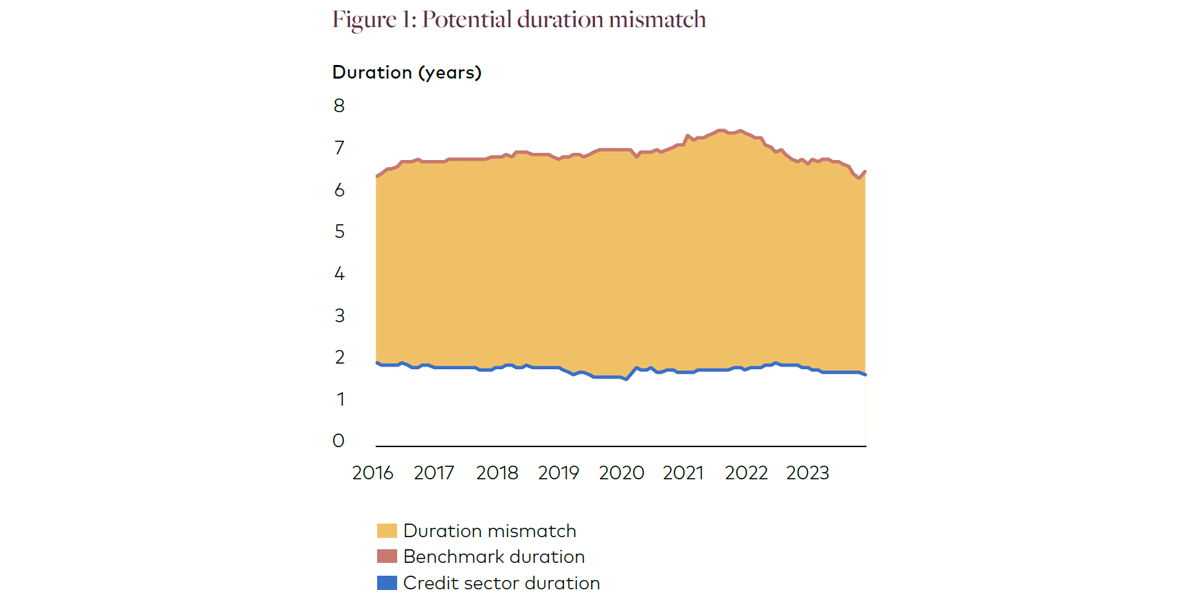

Credit sector construction can cause duration mismatch1

Fixed income sectors may invest across structures, public and private markets, and credit ratings. This flexibility allows investors to exploit a range of investment opportunities but may lead to unintended duration tilts. For example, the chart shows the mismatch between a commonly used fixed income benchmark and an off-benchmark asset mix that invests in corporate debt and leveraged loans.2

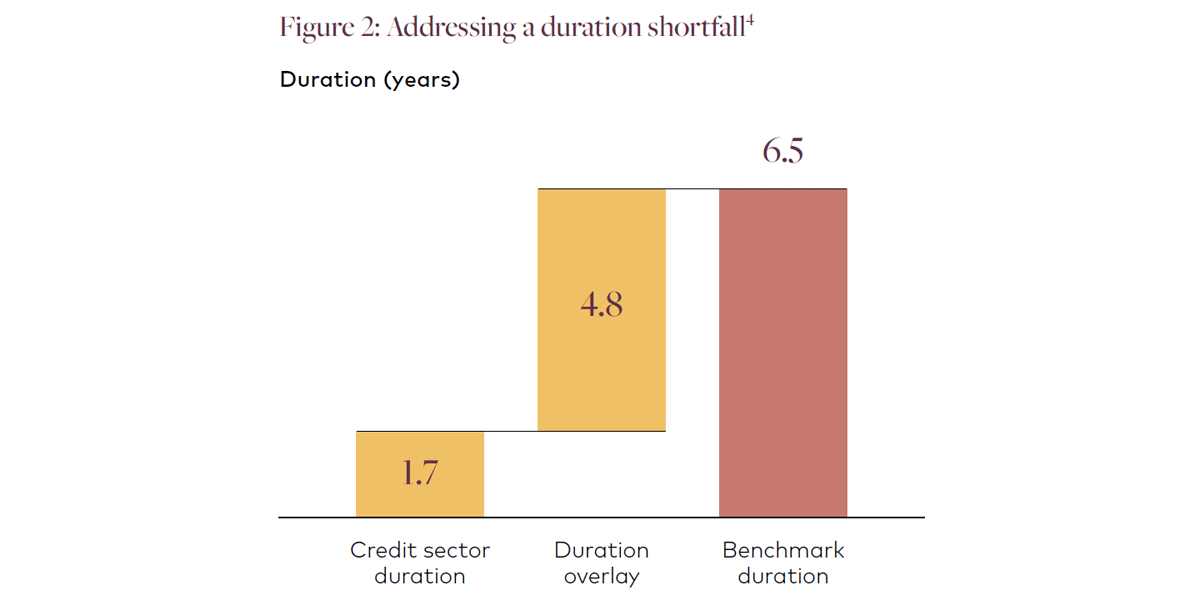

This mismatch can be hedged using a duration overlay

A duration overlay can be used to adjust overall portfolio duration. This reduces duration risk and can provide a better alignment with the relevant benchmark3. The overlay can be constructed using liquid futures contracts and requires only partial funding, making it capital efficient. The chart shows how a duration shortfall can be addressed using a duration overlay.

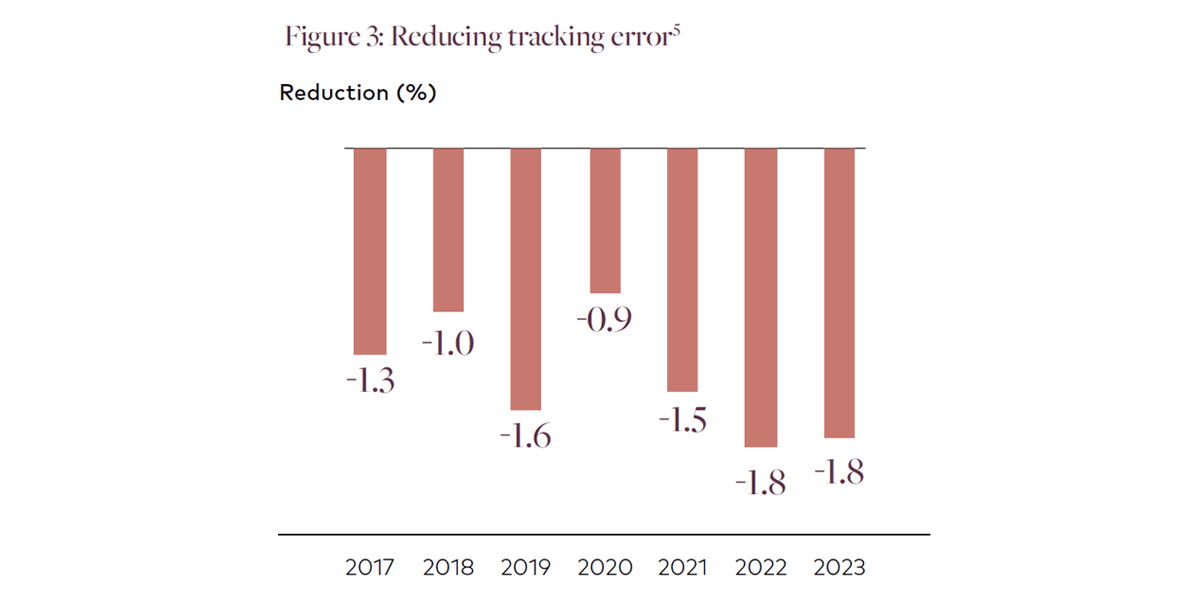

A duration overlay can reduce duration risk and tracking error

A duration overlay can be used to adjust overall portfolio duration. This reduces duration risk and can provide a better alignment with the relevant benchmark3. The overlay can be constructed using liquid futures contracts and requires only partial funding, making it capital efficient. The chart shows how a duration shortfall can be addressed using a duration overlay.

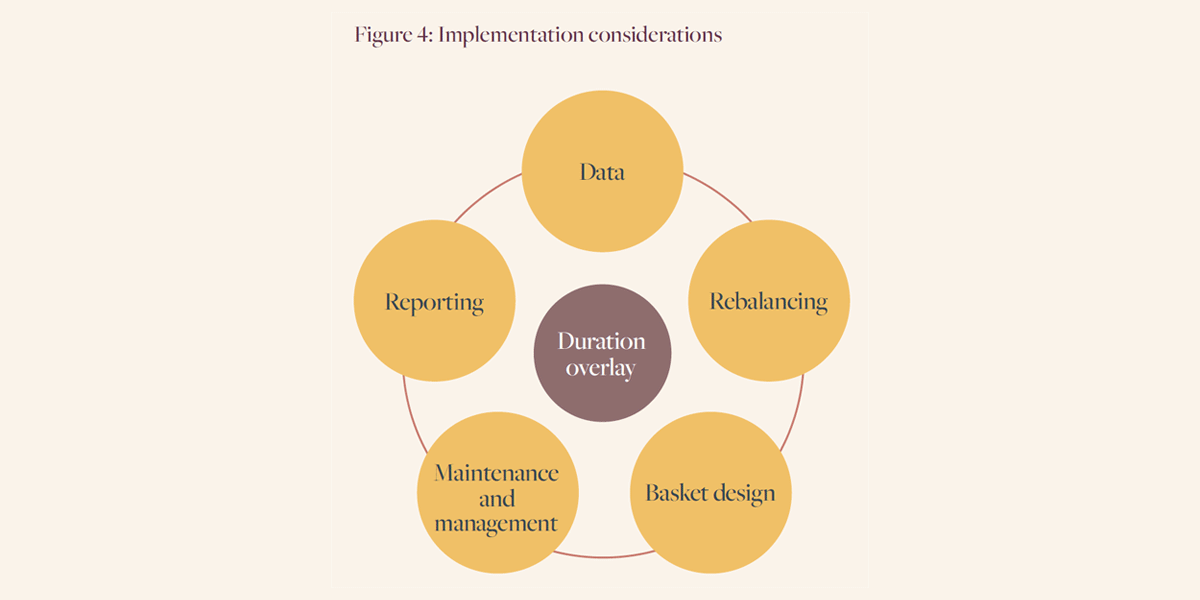

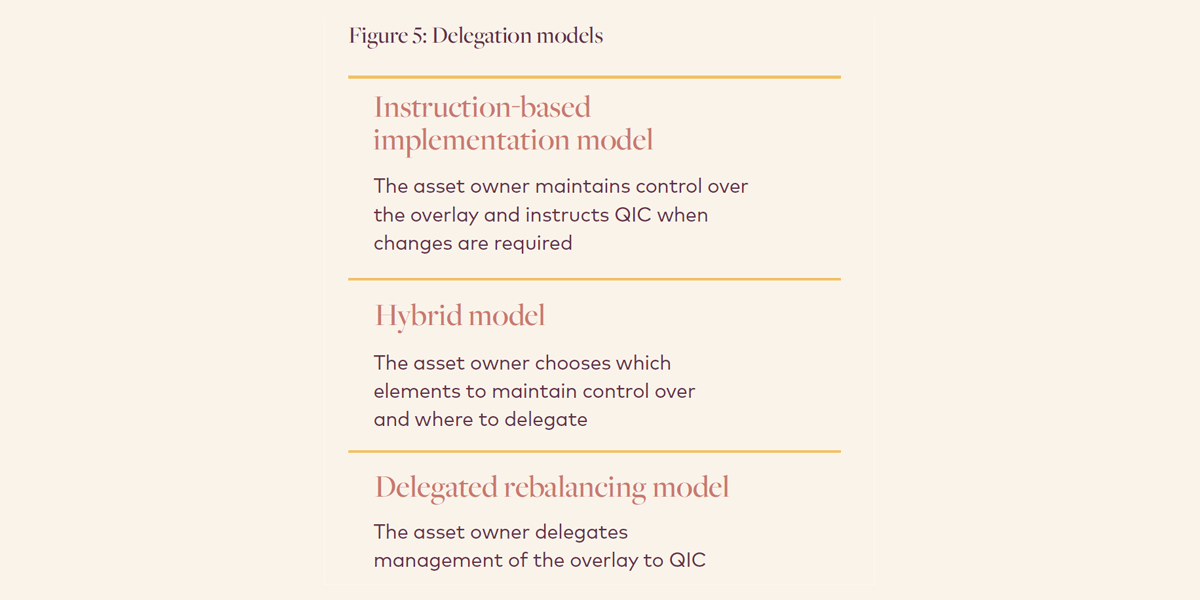

Managing a duration overlay

A duration overlay is typically constructed using a basket of bond futures. These are widely traded, highly liquid instruments that are available across a range of countries and tenors. The variety of available futures contracts allows the overlay to be customised to suit a range of different scenarios and objectives. For example, the country exposures and key rate durations of the overlay can be customised to provide an optimal risk management solution. Various factors should be considered when implementing a duration overlay.

- Data: What informaiton is available to design and manage the overlay?

- Maintenance and management: How often is the basket updated and traded?

- Basket design: What futures and weighting scheme is used?

- Rebalancing: How frequently are positions adjusted to target?

- Reporting: What information about the overlay is required?

Citations

- Source: Bloomberg, S&P, QIC. Date as at 31 December 2023.

- Benchmark is Bloomberg Global Aggregate Index.

- Benchmark is Bloomberg Global Aggregate Index.

- Source: Bloomberg, S&P, QIC. Date as at 31 December 2023.

- Source: Bloomberg, S&P, QIC. Data for the period 31 December 2016 to 31 December 2023.

- As at 31 December 2023.

Past performance is not a reliable indicator of future performance.

Further information

With a 20+ year track record of delivering better investment outcomes for our clients, we partner with our clients to manage more than A$23 billion in cash and fixed income assets, and A$86 billion in derivatives exposures6. Our team has the specialist skills and deep experience to manage the full spectrum of liquid market investment solutions, including cash and fixed income, a broad set of multi-asset derivative solutions and implementation.

QIC Limited ACN 130 539 123 (“QIC”) is a wholesale funds manager and its products and services are not directly available to, and this document may not be provided to any, retail clients. QIC is a company government owned corporation constituted under the Queensland Investment Corporation Act 1991 (QLD). QIC is also regulated by State Government legislation pertaining to government owned corporations in addition to the Corporations Act 2001 (Cth) (“Corporations Act”). QIC does not hold an Australian financial services (“AFS”) licence and certain provisions (including the financial product disclosure provisions) of the Corporations Act do not apply to QIC. Other wholly owned subsidiaries of QIC do hold AFS licenses and are required to comply with relevant provisions of the Corporations Act. QIC also has wholly owned subsidiaries authorised, registered or licensed by the United Kingdom Financial Conduct Authority (“FCA”), the United States Securities and Exchange Commission (“SEC”) and the Korean Financial Services Commission. For more information about QIC, our approach, clients and regulatory framework, please refer to our website www.qic.com or contact us directly.

To the extent permitted by law, QIC, its subsidiaries, associated entities, their directors, officers, employees and representatives (the “QIC Parties”) disclaim all responsibility and liability for any loss or damage of any nature whatsoever which may be suffered by any person directly or indirectly through the provision to, or use by any person of the information contained in this document (the “Information”), including whether that loss or damage is caused by any fault or negligence or other conduct of the QIC Parties or otherwise. Accordingly, you should not rely on the Information in making decisions in relation to your current or potential investments. This Information is general information only and does not constitute financial product advice. You should seek your own independent advice and make your own independent investigations and assessment, in relation to it. In preparing this Information, no QIC Party has taken into account any investor’s objectives, financial situations or needs and it may not contain all the information that a person considering the Information may require in evaluating it. Investors should be aware that an investment in any financial product involves a degree of risk and no QIC Party, nor the State of Queensland guarantees the performance of any QIC fund or managed account, the repayment of capital or any particular amount of return. No investment with QIC is a deposit with or other liability of any QIC Party. This Information may be based on information and research published by others. No QIC Party has confirmed, and QIC does not warrant, the accuracy or completeness of such statements. Where the Information relates to a fund or services that have not yet been launched, all Information is preliminary information only and is subject to completion and/or amendment in any manner, which may be material and without notice. It should not be relied upon by potential investors.

Past performance is not a reliable indicator of future performance.

This Information is being given solely for general information purposes. It does not constitute, and should not be construed as, an offer to sell, or solicitation of an offer to buy, securities or any other investment, investment management or advisory services, including in any jurisdiction where such offer or solicitation would be illegal. This Information does not constitute an information memorandum, prospectus, offer document or similar document in respect of securities or any other investment proposal. This Information is private and confidential. It has not been and is not intended to be deposited, lodged or registered with, or reviewed or authorised by any regulatory authority in, and no action has been or will be taken that would allow an offering of securities in, any jurisdiction. Neither this Information nor any presentation in connection with it will form the basis of any contract or any obligation of any kind whatsoever. No such contract or obligation in connection with any investment will be formed until all relevant parties execute a written contract and that contract will be limited to its express terms. QIC is not making any representation with respect to the eligibility of any recipients of this Information to acquire securities or any other investment under the laws of any jurisdiction. Neither this Information nor any advertisement or other offering material may be distributed or published in any jurisdiction, except under circumstances that will result in compliance with any applicable laws and regulations.

Investors or prospective investors should consult their own independent legal adviser and financial, accounting, regulatory and tax advisors regarding this Information and any decision to proceed with any investment or purchase contemplated by the Information.

Your receipt and consideration of the Information constitutes your agreement to these terms.

This document contains Information that is proprietary to the QIC Parties. Do not copy, disseminate or use, except in accordance with the prior written consent of QIC.